Historic gold rally: what is driving the price surge?

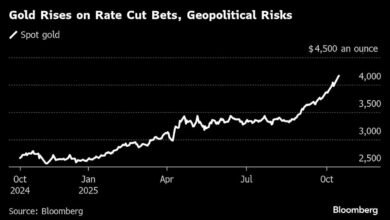

(MarketScreener with Reuters) Gold prices reached a new high on Monday at $3,728 per ounce, extending a spectacular surge that has seen the precious metal double in value since the end of 2022. Buoyed by a climate of geopolitical and economic uncertainty, the gold market is expected to remain under upward pressure in the coming months.

Central banks: massive and sustained purchases

Central bank purchases are the main driver behind this increase, alongside strong investment demand, particularly via gold-backed exchange-traded funds (ETFs). This dynamic is taking place against a backdrop of geopolitical upheaval driven by US President Donald Trump’s foreign policy, his trade wars, and growing questions about the independence of the Federal Reserve.

Since 2022, annual net purchases of gold by central banks have exceeded 1,000 tons, according to Metals Focus. Forecasts for 2025 are still at 900 tons, double the annual average recorded between 2016 and 2021. In particular, emerging countries are seeking to diversify their reserves away from the dollar, after the West froze nearly half of Russia’s foreign exchange reserves in 2022.

According to the World Gold Council (WGC), official data reported to the IMF represents only about 34% of estimated actual demand for 2024. Over the period 2022-2025, central banks contributed 23% of total annual demand for gold, twice as much as in the 2010s.

Jewelry: physical demand declines

Demand for gold for jewelry, traditionally the main component of physical consumption, continues to decline. In Q2 2025, it fell by 14% to 341 tons, its lowest level since the pandemic peak in Q3 2020. This decline is largely attributable to soaring prices, which are deterring buyers, particularly in China and India, two key markets whose combined share has fallen below 50%, a rarity seen only three times in five years.

Metals Focus estimates that gold jewelry manufacturing declined by 9% in 2024 to 2,011 tons and forecasts a 16% drop for the current year.

Bullion and coins: demand remains strong

In the retail investment segment, preferences are changing: bar purchases rose by 10% in 2024, while coin purchases fell by 31%, according to the WGC. This trend is continuing in 2025, although overall demand remains robust.

Metals Focus anticipates a 2% increase in net physical investment this year to 1,218 tons, driven by sustained demand in Asia and continued favorable price expectations.

Gold ETFs: a strong comeback

Gold-backed ETFs have emerged this year as an increasingly important investment channel. Between January and June, these funds recorded net inflows of 397 tons, their best first half since 2020. Total ETF holdings reached 3,615.9 tons at the end of June, a peak since August 2022. The all-time high was five years ago, at 3,915 tons.

Metals Focus forecasts net inflows of 500 tons for 2025 as a whole, following limited outflows of 7 tons in 2024.

In short, despite the decline in jewelry and a transformation of the retail market, strategic demand, whether institutional, geopolitical, or speculative, continues to support a gold market that is more dynamic than ever.

Credit: Source link