(Bloomberg) — Global bond funds have for decades been attracted — and repeatedly burned — by a trade known in Japan as the ‘widow-maker.’

The idea is simple: borrow and sell Japanese government bonds in expectation of tumbling prices, before buying them back and pocketing the difference. The strategy earned its name by piling up losses for debt investors during the country’s long years of ultra-loose monetary policy. Now, it has become one of the most lucrative bets in the global bond market.

Most Read from Bloomberg

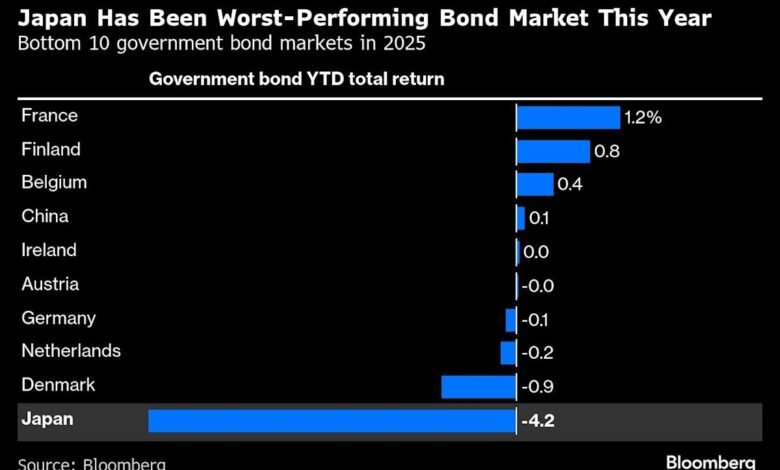

Japanese bonds have lost more than 4% this year in total return terms that exclude currency swings, making them by far the worst performer in the world’s government bond markets, according to Bloomberg calculations. The market has been roiled by on-again, off-again bets on interest rate hikes, and fears that the country’s next prime minister will unleash a spending blitz that could push up long-term yields.

“Forget Treasuries or gilts, one of the cleanest plays is to sell JGBs,” said Mark Nash, money manager at Jupiter Asset Management, of short bets on bonds. “The widow-maker trade has been one of the most profitable relative to other markets.”

Japan’s 30-year bond yields hit an all-time high this month. An S&P gauge of futures linked to the bonds has dropped around 2% this year. The selloff has become so bad that Goldman Sachs Group Inc. has labeled Japan “a net exporter of bearish shocks” in the global debt market.

There are a few key rationales behind the trade. Japan’s core inflation has been above the central bank’s 2% target for almost all of the past three years. Interest rates, despite a series of hikes that started last year, remain exceptionally low in global terms. The trade has also been fueled by broad worries over fiscal policy, which have weighed on bonds from New York to London this year.

Hiroyuki Kimura, portfolio manager at the more than $230 billion Western Asset Management, said his fund has been short duration in Japan’s bond market for a prolonged period and plans to stick to that strategy. The trade is mainly being executed through a large short position in five-year bonds, he said.

WATCH: The “widow-maker” trade has become of the most-lucrative bets in global bonds.Source: Bloomberg

RBC BlueBay Asset Management, which tussled with bond bulls during previous bets on the widow-maker, recently positioned for a decline in Japan’s 10-year bond prices and is now short duration in the country, said Mark Dowding, its chief investment officer for fixed income, in a note on Oct. 10. He still sees value in long-dated yields.

There are risks to the trade. Local life insurers may return at year-end, boosting demand, while improving finances offer some room for the government to reduce issuance in the next fiscal year. US interest rate cuts could offer further support, since Japanese bonds are historically correlated with Treasuries.

But right now, many bond funds remain convinced that Japan’s widow-maker trade will continue to be a rainmaker.

Political Turmoil

A key question for traders is what sort of impact Japan’s next prime minister has on the country’s $7.7 trillion debt market.

Sanae Takaichi, who won the parliamentary vote to become Japan’s prime minister on Tuesday, has promised cash hand-outs and tax cuts but traders also think her ascent will delay rate hikes. That has fueled fears that longer-term bonds will ultimately take the brunt of the selling pressure, as investors worry that future generations will pay the price of fiscal largess today.

Just days after Takaichi won the leadership vote in the Liberal Democratic Party, the governing coalition collapsed — plunging the country into its biggest political crisis in decades. She had secured a new partnership to form an alliance but the risk that political headlines weigh on bonds is far from over.

Yields on Japan’s five-year notes fell two basis points to 1.22% on Tuesday, after Bloomberg reported that Bank of Japan officials see no urgency to hike rates next week.

“We expect there is a deal to be done on fiscal stimulus, although the size of any spending is unclear,” said Lauren van Biljon, senior portfolio manager at Allspring Global Investments UK Ltd., before the new coalition was agreed. “It suggests caution is warranted when it comes to duration in Japan. The yield curve is steep but that doesn’t mean it can’t be steeper.”

Some investors are optimistic. Japanese bond yields are attractive on a hedged basis, making them appealing for many foreign investors, said Kathy Jones, chief fixed income strategist at Charles Schwab & Co. The country’s fiscal position looked to be improving leading up to the elections, which boosts the outlook for the nation’s debt, she said.

The bears may also be overstating Takaichi’s ability to unleash large-scale stimulus, given the risk of a revolt by so-called bond vigilantes — who were partly credited with toppling the brief government of former British Prime Minister Liz Truss three years ago.

“If Takaichi is in any doubt, she should ask the UK what happens when you defy the bond markets,” said Alex Everett, a fund manager at Aberdeen.

What Bloomberg Strategists Say…

“Japanese bond traders are set to target the longest part of the yield curve for strategies to benefit from steady to declining yields. That sets up the risk of another widowmaker pain trade for investors who have been shorting super-long JGBs.”

Mark Cranfield, Markets Live Strategist

But the numbers are stark. Japan has the highest government debt-to-GDP ratio in the developed world by a wide margin. Debt auctions, while showing some signs of easing pressure, remain under heavy scrutiny as yields linger at multi-year highs. The yen is also the worst-performing Group-of-10 currency against the dollar over the past six months despite prospects of further BOJ hikes.

“It’s difficult to see anything other than a continuation of this trend during the remainder of the year, particularly following the Takaichi election victory,” Matthew Ryan, head of market strategy at financial services firm Ebury, said of selling Japanese bonds.

(Adds Takaichi’s victory in parliamentary vote in the 12th paragraph and bond market moves in the 14th paragraph.)