Fiscal consolidation = electoral poison? The global government bond market is suffering from ‘political premium’.

① Signs indicate that global bondholders are currently demanding higher yield premiums for government bonds in developed countries; ② Recent political turmoil in France and Japan highlights how political factors are replacing central bank policies as the main drivers of markets worldwide…

Cailian News, October 14 (Edited by Xiaoxiang) – Signs indicate that global bondholders are currently demanding higher yield premiums for government bonds in developed countries, as recent political turmoil in France and Japan highlights how political factors are replacing central bank policies as the main drivers of markets worldwide…

Last week, after French Prime Minister Gabriel Attal resigned amid a budget deadlock, risk indicators in the French bond market surged to their highest levels this year. However, Attal was quickly reappointed as Prime Minister late on Friday.

In Japan, following the unexpected leadership takeover by Sanae Takaichi within the Liberal Democratic Party (LDP), which triggered concerns over fiscal expansion, long-term Japanese government bond prices plummeted. Last Friday, the ruling coalition between the LDP and Komeito, which had lasted for 26 years, officially collapsed.

Clearly, the latest political turbulence across the globe is no stranger to many bond traders: “Bond vigilantes” are demanding fiscal consolidation from governments, but any similar austerity measures could provoke political controversy and become “political poison” during elections.

Chris Iggo, Chairman of AXA SA Sponsored ADR Investment Management Institute, pointed out: “Both geopolitical risks and political risks are rising, and the situation will only worsen going forward. Political risk will remain persistently high over the next decade.”

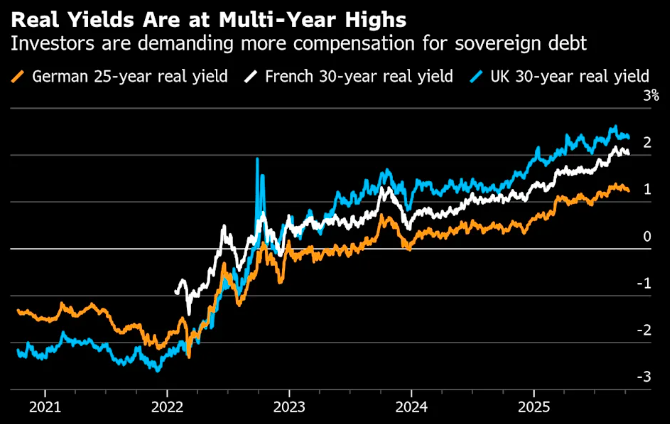

In many regions, inflation-adjusted bond yields—also known as real yields—have recently climbed to new highs. Christoph Rieger, Head of Rates and Credit Research at Commerzbank, noted that this reflects both ‘rising political risks’ and stems from the growing debt issuance needs of various governments.

He warned that long-term real yields in several top credit-rated countries, including Germany, Italy, France, and the United Kingdom, are now significantly higher than their potential economic growth rates.

“Investors need to be vigilant about vicious cycles that may jeopardize debt sustainability,” Rieger stated. “The pain may intensify until painful adjustments are completed and a new sustainable equilibrium is formed.”

In the UK, government borrowing costs are currently the highest among major developed markets, with gilt investors preparing for the Labour Party’s submission of the budget proposal to Parliament by the end of November. Officials are striving to find solutions to fill a fiscal gap of £35 billion (approximately $46.6 billion) while avoiding breaches of politically sensitive tax commitments made during the last general election.

AXA SA Sponsored ADR’s Iggo pointed out that investors in France and the UK generally believe that “the government lacks the governance capacity to push for necessary structural reforms, cut expenditures, and increase taxes,” and that “the political landscape is overly fragmented.”

On Monday, the yield spread between French and German 10-year government bonds remained close to a high of 83 basis points, as Le Cornu was intensifying preparations to submit a highly contentious budget proposal to the new cabinet this week.

For investors such as Lauren van Biljon, Senior Portfolio Manager at Allspring Global Investments, the current backdrop suggests a continued steepening of the global government bond yield curve.

Even in Japan—where its yield curve is already significantly steeper than those of the UK, the US, and France—van Biljon believes there is still room for further steepening of Japanese government bond yields. The sudden collapse of Japan’s ruling coalition has plunged the country into one of its most severe political crises in decades. “The ongoing uncertainty makes me cautious about holding excessive duration in Japanese bonds, even though long-term yields are currently high.”

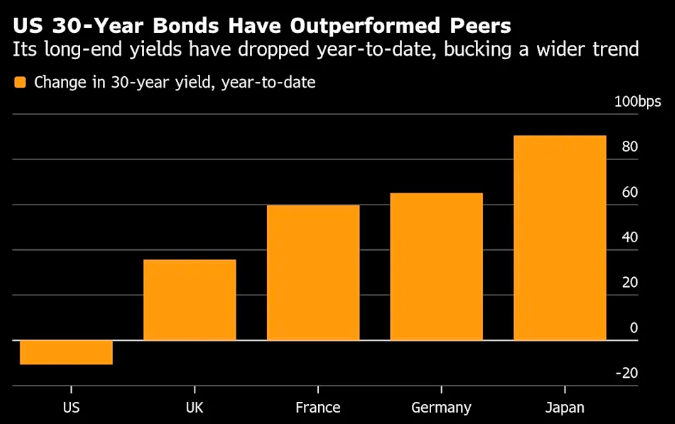

Of course, amid the current pressure on global sovereign bonds, the US Treasury market has been unusually ‘subdued.’ American investors seem to have broadly accepted the heightened uncertainty because the elevated yields themselves already provide sufficient compensation.

At the same time, despite unprecedented erosion of the US political environment—with a government shutdown depriving investors of key data—the US Treasury market retains its safe-haven status amid significant volatility. The dollar also just concluded its strongest weekly performance in nearly a year.

George Catrambone, Head of Americas Fixed Income at DWS Group, who purchased long-dated US Treasuries at higher yields over the past few months, has recently adopted a neutral stance toward the yield curve.

He stated: “There is no flight-to-safety behavior evident in US Treasuries. US assets still maintain a certain exceptionalism. When looking at fiscal issues in Japan, France, and the UK, where else can investors turn?”